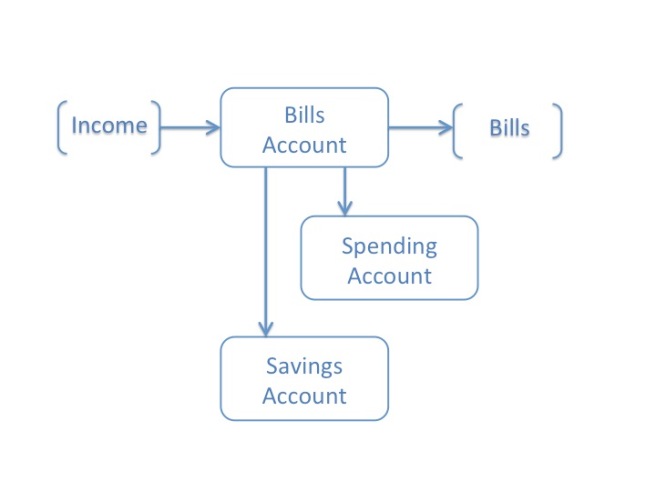

The money management system that I recommend to “fallible humans” like me is the three-account “Jam Jar” system I described in an earlier post. I’ve also talked about how to set up a separate Spending Account here. In this post we’ll look at the final piece of the puzzle – setting up a Savings Account. Here’s how they fit together:

Why save?

Our spending tends to be “lumpy”. On top of our regular outgoings we also spend relatively large amounts at irregular intervals, whether it’s planned spending on a summer holiday, or unplanned but essential spending on a replacement washing machine. And these lumps in our spending don’t match our income. So where are we going to find the money?

Most of us have a simple choice – we can either pay for this lumpy spending out of savings or out of debt – typically by putting it on the credit card. Now debt is much easier to get into than to get out of. So whether you want to avoid getting into debt, or you’re trying to get out of debt, the best way to help yourself is to start saving regularly. Cultivating a savings habit is essential to your financial wellbeing.

Make a commitment

If you’re not saving already, now is the time to start. So go back to your budget, and add a line for monthly savings. Decide how much you can afford to save each month. It doesn’t matter how much – £10 or £100 – so long as you commit to saving something every month, starting now. You can always increase this amount later, perhaps when you get a pay rise or you finally manage to pay off that credit card.

Choosing a Savings Account

Saving takes discipline and will power, which is always in limited supply, and can run low just when we need it. So it makes sense to bolster our will power with commitment devices – self-imposed barriers which we can use to make it harder for us to deviate from our commitment. For example, if I’m on a diet, I don’t buy chocolate and keep it in the cupboard. If I’ve given up alcohol, I invite my friend to meet me in a coffee shop, instead of a pub. Money management for fallible humans works the same way, so I suggest you choose a savings account with the following two features:

1.Save by standing order: Make sure you can pay into your Savings Account just like paying any other bill. Set up a monthly standing order for the amount you’ve committed to save so it comes out of your Bills Account before you transfer whatever’s left into your Spending Account. Don’t spend all month trying not to spend all your money so you can save whatever’s left. Do your saving first, not last.

2. Ease of access: this is probably the most important feature of a Savings Account – it shouldn’t be too easy to access. So make sure your savings account is not too close to your spending account. I have several accounts with Barclays and I can see them all at the same time on my banking app. With a couple of taps I can instantly move money between accounts. When I had my Spending Account with Barclays this was a real problem – when I ran short of spending money, it was just too easy to transfer money out of my Savings Account. So I moved my Spending Account to a Monzo prepaid debit card. When my Monzo balance gets low, it’s no longer easy to dip into my Savings Account.

But ease of access when you really need it is still important, so using an instant access account will enable you to draw your “rainy day” savings out at short notice without paying a penalty.

Set Goals

It’s a very good idea to set yourself a Savings Goal – and reward yourself in some way when you reach your Goal. In my last post I suggested that every household should aim to have at least £1,000 of “rainy day” savings. If that sounds too challenging, then aim for £500. If you’re well on the way, then you might want to start saving for other things, so you should consider using a specially designed savings account that will allow you to set multiple savings goals and keep track of how your doing, all within a single account.

The Fairbanking Foundation independently tests banking products to find out just how helpful they are to consumers. Only one Savings Account has achieved their highest award – a 5 star Fairbanking Mark – and that’s the Instant Saver Account with Savings Goals offered by NatWest. Here are some of the features which earned it a 5 star award:

- You can set up one or more goals or savings ‘pots’

- You can set up a specific “rainy day” fund for emergencies

- You can find out how much you will need to save and for how long

- You can easily set up a regular payment into your saving account

- You can easily see how you are progressing towards your savings goals

The aim of this blog is to make your life simpler, so if you already have a savings account set up which is working fine and is not too easy to access, then you don’t need to set up another one. But a specialist account like this one is worth considering if you’re starting from scratch, or if you’re already saving up for more than one goal.

What about the rate of interest?

The NatWest Savings Account described above pays interest of 0.01% per annum – that’s as close to zero as makes no difference. But the Fairbanking Foundation has still given it a 5 star award. That’s because the positive features of this product will contribute much more to a customer’s ability to achieve their savings goals than earning a slightly higher rate of interest.

It’s the money that you yourself save that makes all the difference, and not the little bit of interest on top. If you do manage to build a rainy day fund of £1,000 then earning an extra 1% of interest would add an extra 83 pence per month to your savings. So unless you’ve got a lot of money saved up (i.e. over £10,000) then all the other factors I talk about in this post are going to be much more important to your ability to save than the rate of interest.

Financial wizards might care about the rate of interest – but it’s really not that important to the “fallible humans” I’m writing this blog for.

Very good advice Rob. I was brought up to save – my father worked in insurance.

LikeLiked by 1 person

Thank you Allison. If only we had all been taught to save like you! It’s not an easy habit to acquire when the going gets tough.

LikeLike

Another great blog, and a good read, I think the challenge I face currently and what I need to do is to work out the spending like car serice and MOT testing, and those things and then account for those in my bills account, as a pose to dipping into the savings. Is that what you would recomend? The bills account is really working for me.

LikeLike

Your annual car service and MOT bill is a good candidate for the bills account as you know when you’ll have to pay it and approximately how much it will be. So you can plan for it and save for it in your bills account. It’s more motivating to use you savings account to save for things that you can look forward to – like a family holiday.

LikeLike